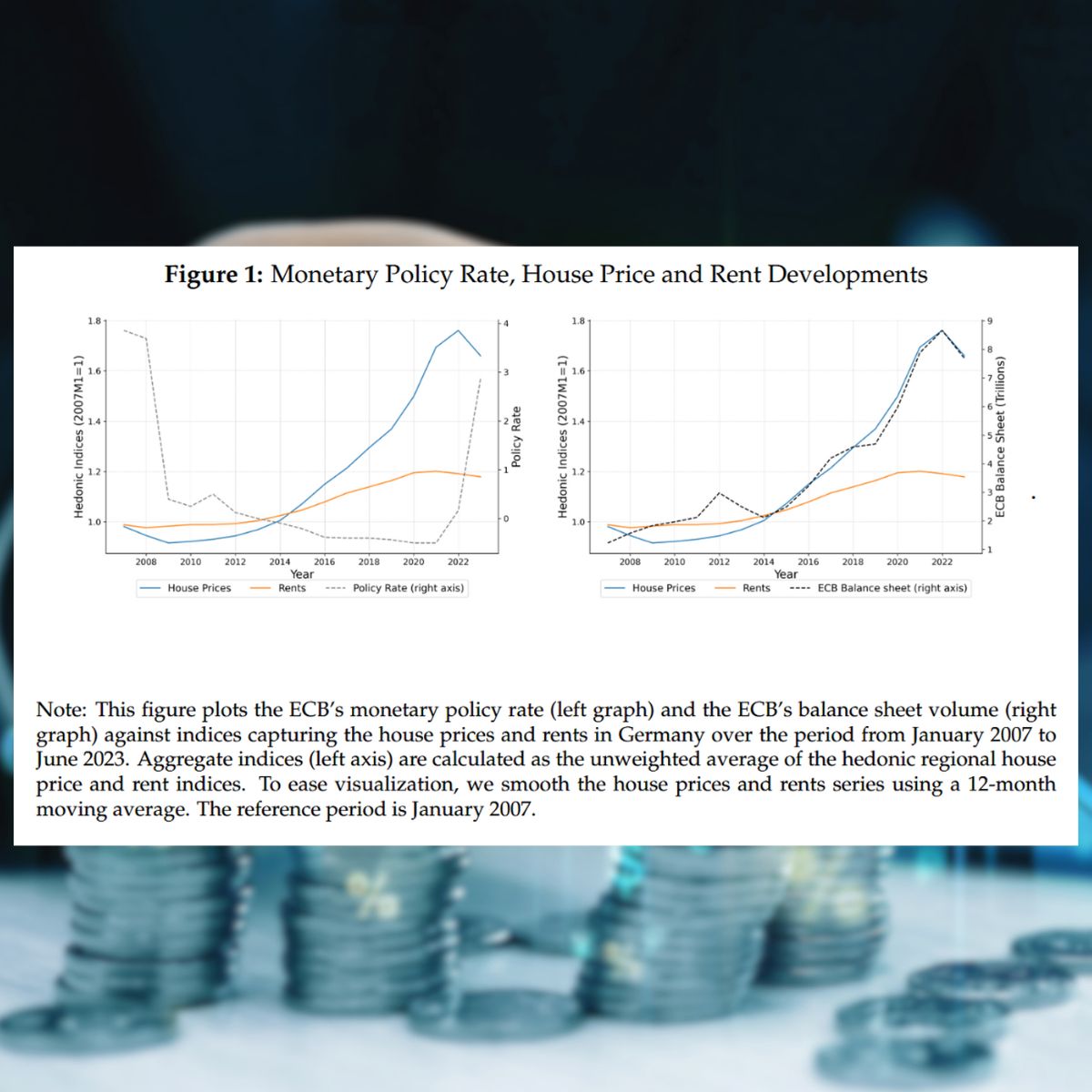

Monetary policy plays a crucial role in shaping economic conditions, but its impact on the housing market is often overlooked. A recent study by Martin Groiss and Nicolas Syrichas explores how central bank policies—particularly interest rate cuts and unconventional measures like quantitative easing—affect house prices and rents in Germany. By analyzing 35 million real estate listings from 2007 to 2023, the study provides new insights into how monetary policy decisions translate into changes in the housing market. The findings raise important questions about affordability and financial stability.

When the European Central Bank (ECB) lowers interest rates, borrowing becomes cheaper. This makes mortgages—long-term loans used to buy homes—more affordable, encouraging more people to purchase property. At first glance, this seems like a positive outcome. More individuals and families can afford a home, and lower financing costs make real estate investments more attractive. However, this increase in demand does not automatically lead to more homes being available. Housing supply—meaning the number of homes for sale—takes time to adjust. Construction projects can take years, and in cities with strict zoning laws or limited space, the number of new homes built remains relatively low. As a result, when more people rush to buy homes but the number of available properties remains the same, prices rise.

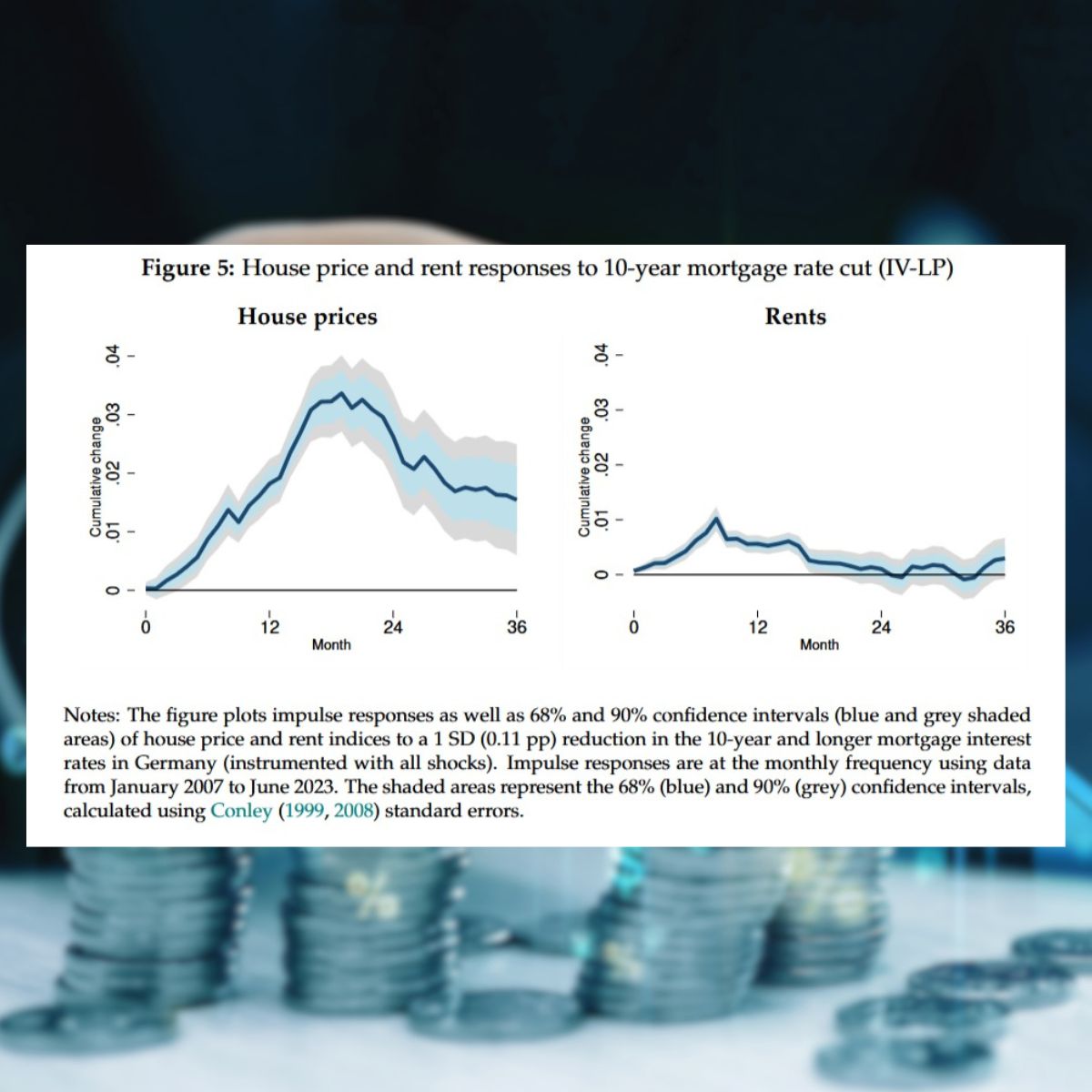

The study finds that house prices do not just increase slightly after an interest rate cut—they rise significantly and stay high for several years. In contrast, the effect on rents is much weaker. While rents do increase, the study finds that their growth is less immediate and less persistent than house price increases. One key reason for this is the way housing demand shifts after a monetary policy change. The study shows that when borrowing becomes cheaper, many renters move into homeownership, increasing demand for homes for sale rather than for rental units. This movement slows down rent growth.

Another key factor driving price increases is the behavior of existing homeowners. The study finds that when interest rates are low, fewer people who already own a home decide to sell. If someone has a mortgage with a low fixed interest rate, they are less likely to move because selling their home would mean giving up their favorable loan conditions. Even if they consider moving, they might hesitate because taking out a new mortgage in the future—even at a still relatively low rate—could still be more expensive than their current loan. This means that fewer homes enter the market, further reducing supply. The result is that even as more buyers enter the market, fewer homes are available, which pushes prices even higher.

This creates a particular challenge for new buyers and renters trying to transition into homeownership. While low interest rates theoretically make mortgages more affordable, the reality is that house prices rise so much that this benefit is canceled out. A first-time buyer, for example, may find that while their monthly mortgage payments would be low, the initial down payment required to buy a home becomes much larger as prices increase. Since renters do not accumulate home equity the way homeowners do, it becomes increasingly difficult for them to save enough to enter the market. In the long term, this can widen the gap between homeowners and renters, creating inequalities in wealth accumulation.

What can be done about this? The study suggests that monetary policy alone cannot address housing affordability issues. While lower interest rates stimulate economic growth, they also create unintended consequences in the real estate sector. Policymakers may need to complement monetary policy with targeted housing measures, such as incentives for new housing construction, support for first-time buyers, or regulations to prevent excessive real estate speculation. Without such measures, low interest rates may continue to benefit those who already own property while making it harder for new buyers to enter the market.

The findings of this study highlight the need for a balanced approach to monetary and housing policies. While central banks focus on stabilizing the economy as a whole, the impact on individual markets—such as real estate—should not be ignored. The challenge remains: how can we ensure that monetary policy supports growth while also keeping housing affordable for future generations?

On the Authors

Martin Groiss

Postdoctoral Researcher in Macroeconomics at the University of Duisburg-Essen. He earned his PhD from Goethe University Frankfurt in 2024 and has held visiting positions at the ECB and Bundesbank. His research focuses on monetary policy, labor markets, and environmental economics, using empirical methods and granular data analysis.

Nicolas Syrichas

Postdoctoral Researcher at Freie Universität Berlin and a member of the Berlin School of Economics. He earned his PhD in Economics from Goethe University Frankfurt in 2023 and specializes in monetary policy, labor markets, and macroeconomics. His research combines quantitative models and large-scale microdata to analyze economic dynamics. Before joining FU Berlin, he was affiliated with the Frankfurt Quantitative Macro Group.