After more than two months of restrictions due to the Covid-19 pandemic, many households are facing severe financial challenges. Job loss, pay cuts, and other adverse effects are straining household finances. Government assistance is being provided in many places, but it is usually insufficient to restore pre-crisis income levels. This leaves households reliant on personal savings (or new loans) to smooth consumption.

Household income (relative to expenses) remains the critical factor explaining whether one can accumulate sufficient savings for emergencies. Still, another important attribute standing out is financial literacy. This term includes the set of skills needed to be able to cope with financial problems.

Financial literacy is linked to many desirable financial behaviors. For instance, US survey data show that financial knowledge is associated with a significantly higher probability of having emergency funds sufficient to finance three months of typical expenditures, controlling for many explanatory variables including income (Babiarz and Robb, 2014). However, low levels of financial literacy are simultaneously found to prevail across countries (Lusardi and Mitchell, 2014).

There is evidence that these considerations are also likely to be valid in Germany. Using data from the SOEP innovation sample (IS) 2018 wave, we can show that household heads with higher financial literacy took significantly more precautionary financial measures for their households. The survey data were collected about one year before the Covid-19 pandemic hit Germany. It seems reasonable to assume that the financial behavior observed then significantly affects how households maneuver through the crisis right now.

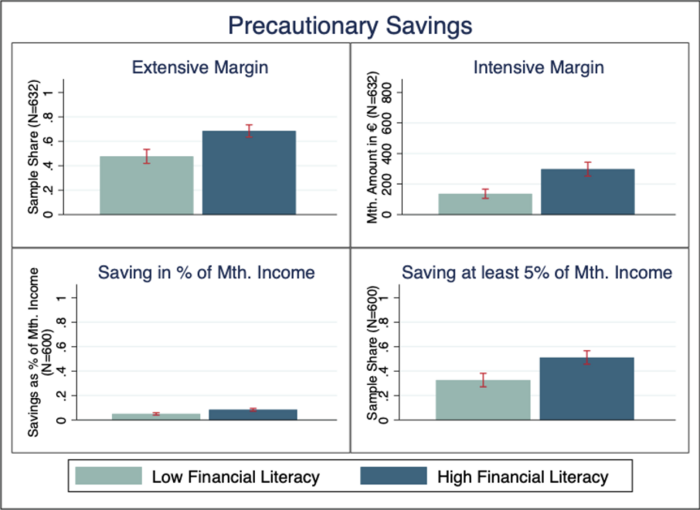

The SOEP-IS household survey uses a rather rich measure for financial literacy with six questions assessing the financial knowledge of each respondent. Worryingly, we find – in line with other surveys - that about 35 percent of all respondents cannot save on a regular basis. To inspect the potential relevance of financial literacy for savings behavior, we create a standardized score out of these questions, dividing the sample into having below and above median financial literacy. We then compare the two groups by their propensity to save and the absolute and relative amounts they save for precautionary reasons.

The above median financially literate persons have a 21 percentage points higher likelihood of regularly saving for precautionary reasons. This result is displayed in the below figure as the extensive margin and is statistically significant at the 1 percent level. The amount of money saved is also significantly higher among the more financially literate. Moreover, they are almost twice as likely to save the recommended 5 percent of their monthly income as buffer for times of crisis. Other forms of savings, such as retirement and investment funds, are likely not as flexible and helpful at the moment. However, when including them in an analysis, we find the same results.

All of these differences cannot be explained by differences in income in general, as we control for net household income in additional linear regressions and the results virtually do not change.

It seems that in Germany, individuals with higher financial literacy are financially better prepared for an unexpected income shock, like that caused by the coronavirus crisis. This shows that it is crucial for households to have the skills to prepare for crises. Given that only more financially literate individuals, on average, manage to save the minimum recommended amount for rainy days, policymakers should take more action in financial education. Investing in financial education pays off, as shown in a new meta-analysis. Financial trainings have a positive average treatment effect on financial behavior, especially also on savings behavior, and are, typically, cost-effective (Kaiser et al., 2020). Thus, investing in financial literacy makes societies more resilient for crises like the current Covid-19 pandemic.

[insert image]

Copyright Jana Hamdan/Melanie Koch

Notes: Precautionary savings are measured as monthly contributions and include any form of savings the household itself defines as precautionary savings. Monthly income refers to the current monthly household net income. All numbers are reported by the household head. Financial literacy groups are defined over the subsample of household heads, where low financial literacy means below and high financial literacy above median or median financial literacy.

Jana Hamdan (DIW Berlin and HU Berlin)

Melanie Koch (DIW Berlin)

Kaiser, Tim, Annamaria Lusardi, Lukas Menkhoff, and Carly Urban. 2020. Financial Education Affects Financial Knowledge and Downstream Behaviors. NBER Working Paper No. 27057.

Lusardi, Annamaria, and Olivia S. Mitchell. 2014. The Economic Importance of Financial Literacy: Theory and Evidence.Journal of Economic Literature, 52 (1): 5-44. DOI: 10.1257/jel.52.1.5.

Babiarz, Patryk, and Cliff A. Robb. 2014. Financial Literacy and Emergency Saving. Journal of Family and Economic Issues, 35 (1): 40-50. DOI: 10.1007/s10834-013-9369-9.